Institutional Insights: Goldman Sachs 'G10 FX Carry Comeback'

The G10 FX Carry Comeback

The main argument is that carry is more relevant for G10 FX now than at almost any point since 2000. The current setup combines historically elevated outright carry with historically subdued FX volatility, creating unusually attractive carry-to-vol opportunities across G10 currencies. This is especially notable because G10 FX carry has often been less compelling than EM carry, but today the gap between EM and G10 carry opportunities is narrower than usual.

The backdrop is straightforward: post-Covid inflation and the recent energy shock have left G10 policy rates high and dispersed, while the expected path of policy from here is relatively stable. That means rate differentials are large enough to generate meaningful carry, but the volatility around those differentials has declined. In FX terms, that is a powerful combination: investors can earn carry without needing large spot moves, and in many cases spot has actually moved in the same direction as carry this year.

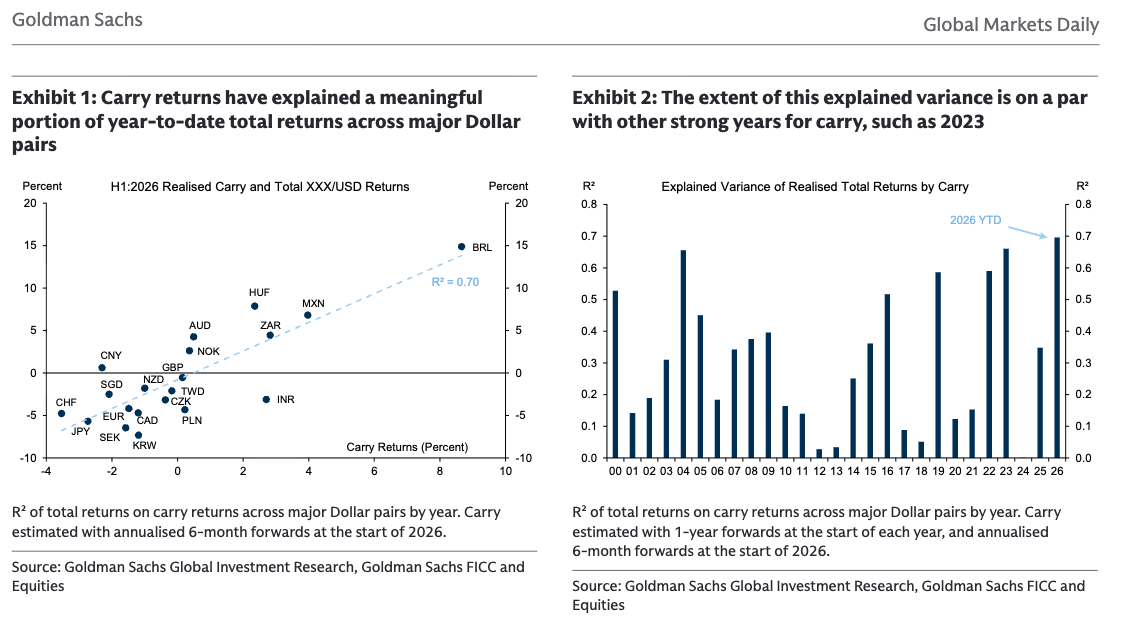

Year-to-date, carry has explained a historically large portion of total returns across major dollar pairs, roughly in line with other strong carry years such as 2023. The relationship has worked both because spot volatility has been muted and because spot moves have been positively correlated with carry. In other words, investors have not just earned the interest-rate differential; they have also often benefited from currency appreciation in higher-yielding currencies. Commodity-linked high yielders have also benefited from the energy terms-of-trade shock.

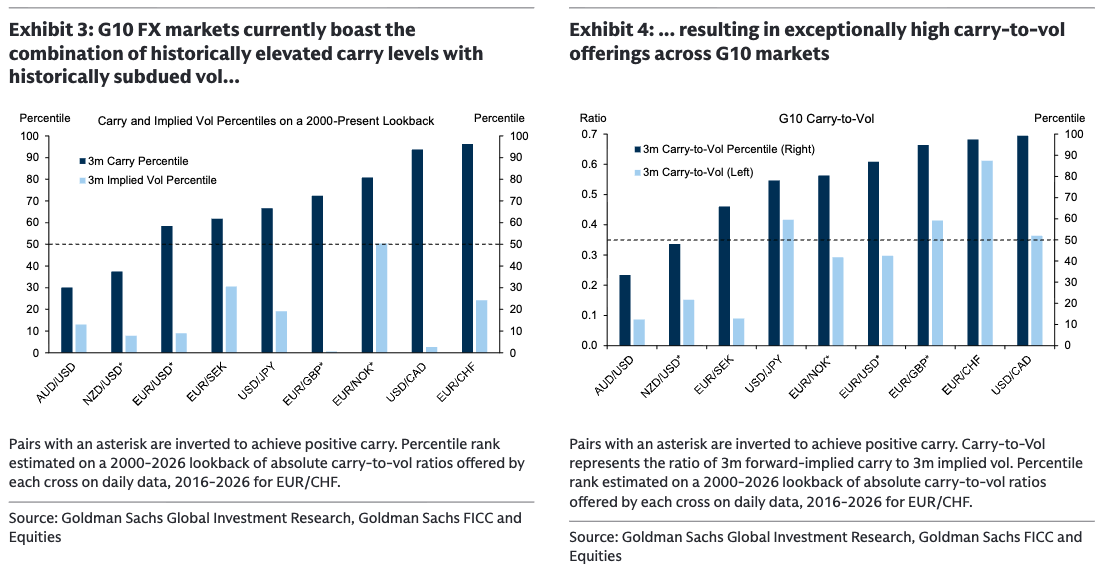

The most important metric is carry-to-vol. G10 FX markets currently offer unusually high carry relative to implied volatility. Crosses such as USD/CAD and EUR/CHF are close to multi-decade highs on 3-month carry-to-vol measures. This matters because carry strategies are fundamentally about earning yield per unit of risk. When carry is high and implied vol is low, the breakeven for spot moves becomes more favorable and the probability of carry dominating total return rises.

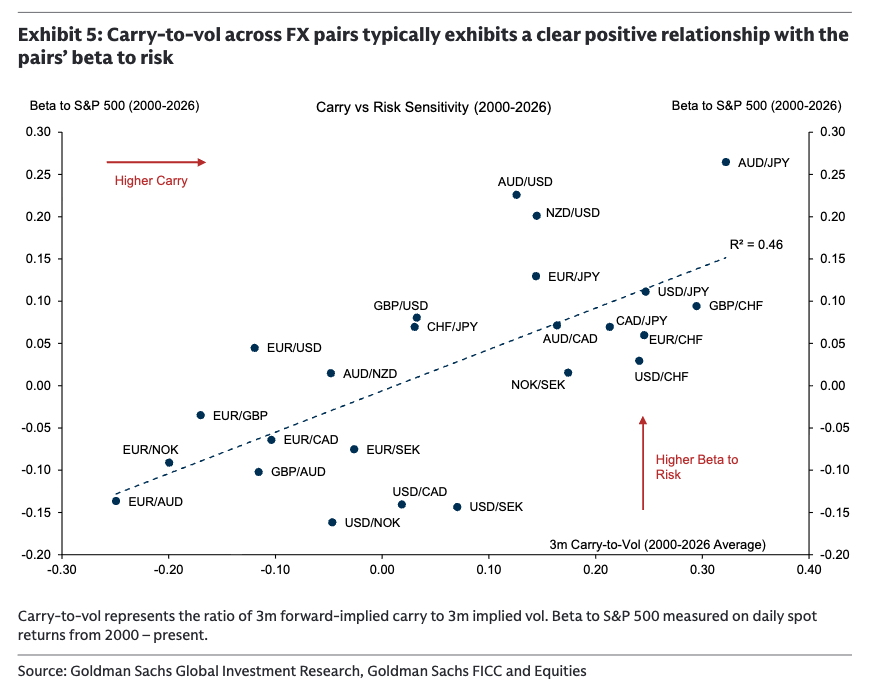

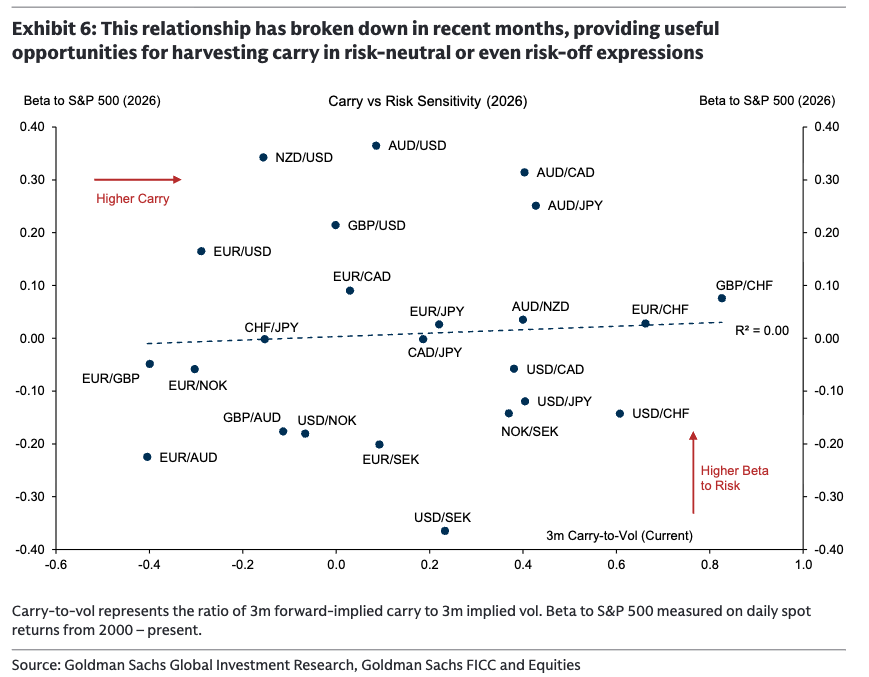

A particularly interesting feature of the current regime is that the traditional relationship between carry and risk beta has broken down. Historically, higher carry usually came with higher sensitivity to risk assets: you earned more carry, but you were effectively long global risk. That relationship has weakened substantially in recent months. As a result, investors can now find attractive carry-to-vol in crosses that have behaved relatively risk-neutral, such as AUD/NZD and EUR/CHF, as well as in trades that may even have risk-off characteristics, such as being long USD versus NZD or SEK.

That is useful in the current multi-asset environment. Equity markets are dealing with AI/momentum de-risking, renewed geopolitical oil risk, higher yields, and rising dispersion. In that backdrop, the ability to earn FX carry while remaining insulated from, or even hedged against, equity drawdowns is valuable. G10 carry is therefore not simply a pro-risk trade; it can be used as a portfolio diversifier if the funding and long currencies are chosen carefully.

EM FX still offers the clearest carry-to-vol opportunities overall, but the relative advantage versus G10 is smaller than usual. This makes G10 carry more attractive for investors who want cleaner liquidity, lower event risk, and more scalable implementation. In particular, the preferred G10 funders remain JPY, CHF, EUR, and CAD, with different advantages and risks attached to each.

JPY remains a top funding currency over longer horizons. Intervention risk is the main tactical concern, but without a change in the fundamental backdrop — higher-for-longer US yields, low recession risk, and lingering Japanese fiscal concerns — the yen is expected to continue weakening steadily. That keeps JPY attractive as a funding currency, even if its carry-to-vol does not screen as especially elevated beyond the 2-month horizon.

CHF is also a favored funder because it remains the lowest-yielding G10 currency by a wide margin. Trades such as EUR/CHF and GBP/CHF currently offer some of the highest carry-to-vol among major crosses and have shown relative insulation from risk in recent months. SNB intervention policy is not expected to be a major obstacle to CHF funding near term. The bigger risk is a renewed gold rally, which could support CHF through terms-of-trade channels and complicate longer-term CHF-funded carry trades.

EUR remains a viable funding option, particularly because it is more liquid than JPY or CHF in many implementations. However, its carry-to-vol offering is less clearly elevated than JPY or CHF. EUR funding is still useful, but it is not the cleanest or highest-conviction expression of the carry theme.

CAD has also been a preferred funding currency this year because it can reduce risk exposure and increase carry relative to USD funding. Ongoing trade uncertainty is expected to continue weighing on CAD via the USD/CAD rate differential. That said, after CAD’s substantial underperformance over the past two months, the additional spot-depreciation upside from short CAD now looks somewhat less compelling.

G10 FX carry is back as a major portfolio theme. The setup of high rate dispersion, stable policy expectations, subdued FX vol, and weakened correlation between carry and risk beta creates an unusually attractive environment for carry strategies. The best expressions are not simply the highest-yielding currencies versus the lowest-yielding ones, but trades with strong carry-to-vol and controlled risk sensitivity. The preferred funding currencies remain JPY, CHF, EUR, and CAD, with CHF and JPY offering the cleanest structural funding cases, EUR offering liquidity, and CAD offering a more risk-reducing funding profile after its recent underperformance.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!